Can You Buy a Home with Credit Challenges or an Unstable Job?

Here’s What Buyers Need to Know

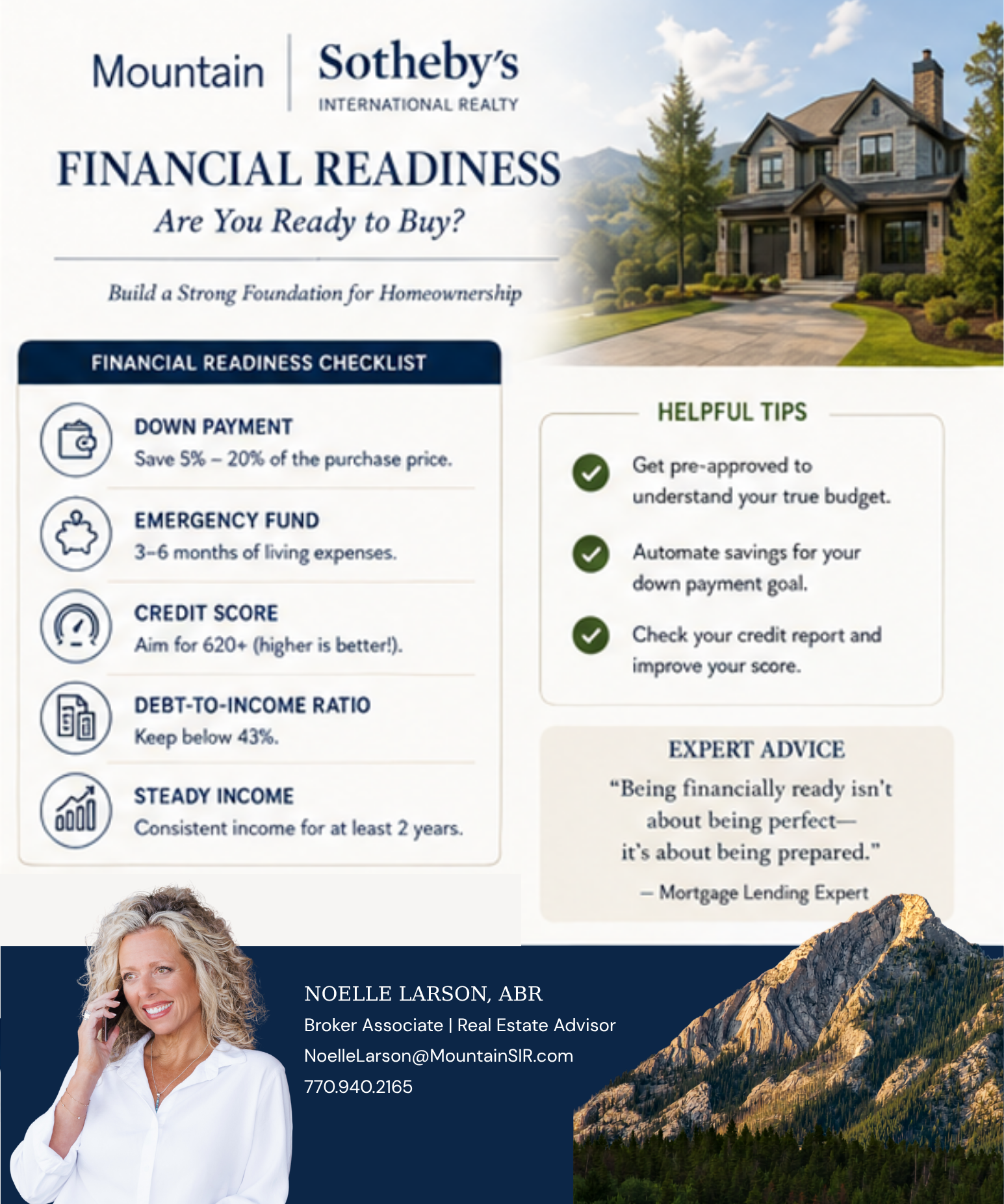

One of the biggest misconceptions in real estate is that buyers need perfect credit, stable salaries, and ideal financial situations before purchasing a home.

In reality, many successful buyers navigate:

Self-employment

Commission-based income

Career transitions

Credit rebuilding

Variable income streams

The key is preparation, documentation, and working with the right professionals.

Can You Buy With Bad Credit?

Yes, depending on the severity of the issues and the loan program.

Lenders Often Consider:

Current credit score

Debt-to-income ratio

Recent payment history

Income stability

Cash reserves

Even buyers with lower scores may qualify for certain financing options.

Buying With Variable or Self-Employment Income

Self-employed buyers often need:

Two years of tax returns

Consistent income history

Profit and loss statements

Bank statements

Preparation and organization are critical.

How Long Should You Be at Your Job?

Many lenders prefer:

Two-year employment history

Stable income patterns

Consistency within the same field

However, changing jobs does not automatically prevent approval. In reality, career advancement moves are often viewed differently than inconsistent employment gaps.

Refinancing Later: What Buyers Should Know

One major advantage of buying now is the ability to refinance later if rates improve.

Refinancing may help:

Lower monthly payments

Reduce interest costs

Shorten loan terms

Access equity

This flexibility allows buyers to focus on securing the right property today while maintaining future financial options.

Expert Advice

Work on Progress, Not Perfection: Even small financial improvements can significantly improve buying power.

Build a Mortgage Strategy Early: Meeting with a lender before you are ready allows time to improve your position.

Keep Documentation Organized: Clear financial records create smoother approvals.

Helpful Tips

Tip #1: Avoid Missing Payments

Recent payment history matters heavily.

Tip #2: Reduce Revolving Credit Balances

This can improve debt-to-income ratios.

Tip #3: Avoid Career Changes Mid-Transaction

Stability helps during underwriting.

Tip #4: Ask About Specialized Loan Programs

Many buyers qualify for programs they never knew existed.

If you are unsure whether you qualify to buy, the best first step is having a conversation.

I am always proud to connect my buyers with trusted lenders in an effort to help create a realistic path toward homeownership. Let’s connect and start the conversation!