Financially Ready to Buy a Home? What Buyers in Georgia Need to Know

Buying a home is one of the biggest financial decisions most people will ever make. Yet many buyers assume they need perfect finances before they can even begin the process.

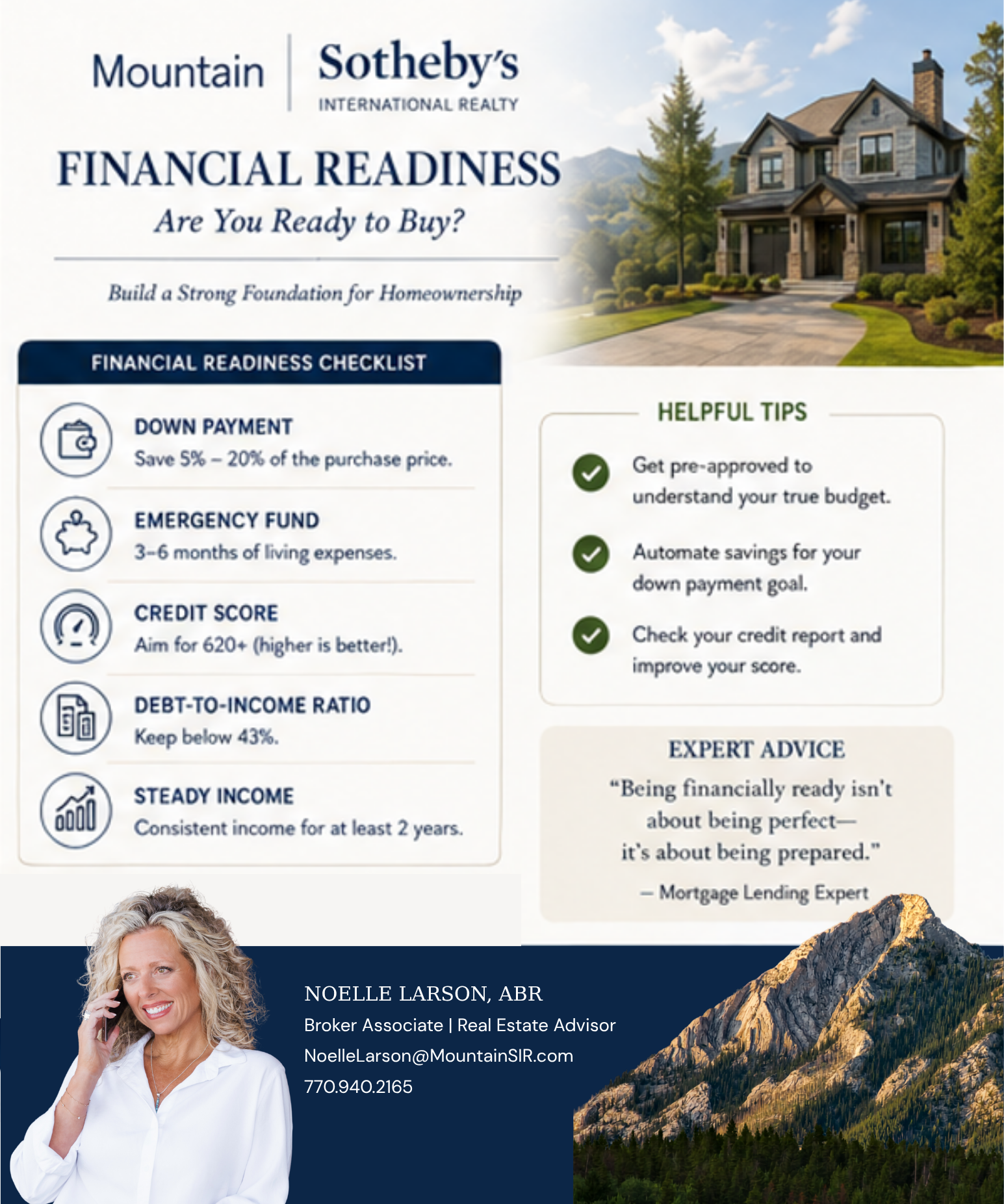

The truth is that financial readiness is not about perfection, it is about preparation, stability, and strategy.

Whether you are purchasing your first home in Canton, upgrading in Alpharetta, or searching for a mountain retreat in Ellijay, understanding your financial picture is the foundation of a confident purchase.

How Much Should You Have Saved?

Typical Expenses to Prepare For

Down payment

Earnest money deposit

Closing costs

Moving expenses

Inspection fees

Emergency savings

Initial home maintenance

Recommended Savings Benchmarks

3–5% minimum down payment for many loan programs

10–20% for stronger purchasing power

3–6 months of emergency reserves

Remember: waiting for a full 20% down payment may not always be necessary.

How Much House Can You Afford?

Affordability is about more than what a lender approves.

A comfortable budget should allow you to:

Save consistently

Enjoy your lifestyle

Handle unexpected expenses

Avoid becoming “house poor”

Experts Often Recommend:

Housing expenses below 28–30% of gross monthly income

Total debt below 36–43% of monthly income

Should You Wait Until Your Income Increases?

Sometimes waiting makes sense.

If you expect:

A major salary increase

Career stability improvements

Debt reduction

Better savings growth

…then delaying may improve your long-term comfort level.

However, buyers should also consider:

Rising home prices

Interest rate changes

Lost equity growth

Continued rent payments

Student Loans & Debt Considerations

Having student loans does not automatically prevent homeownership.

Lenders evaluate:

Debt-to-income ratio

Credit score

Payment history

Income stability

Many successful buyers purchase homes while responsibly managing student debt.

Expert Advice

Build a “Comfortable” Budget, Not a Maximum Budget

Just because you qualify for a payment does not mean you should take on the maximum amount.

Maintain Financial Flexibility

Homeownership should support your life—not create financial stress.

Focus on Monthly Lifestyle

Think about:

Travel

Retirement savings

Childcare

Hobbies

Future goals

Your mortgage should fit into your life comfortably.

Helpful Tips

Tip #1: Improve Credit Before Buying

Even small credit score improvements can lower monthly payments.

Tip #2: Avoid Major Purchases Before Closing

New debt can impact approval.

Tip #3: Get Pre-Approved Early

Understanding your numbers reduces uncertainty.

Tip #4: Work With Local Experts

Local lenders often understand Georgia market conditions and loan programs better.

Not sure if you are financially ready to buy? We help buyers create a clear roadmap that fits both their budget and future goals.

Let’s talk about what a personalized home buying strategy looks like for you.